Q1 2026: A Solid Foundation... with a Shrinking Margin for Error

- David Halseth

- Apr 10

- 8 min read

Updated: Apr 12

For the quarter ending March 31st, 2026.

If you’re looking for a clean read on the economy, the answer is surprisingly straightforward: most indicators still look...pretty good. Growth remains intact, the consumer continues to spend, and inflation - at least for now - has settled into a more manageable range. The notable exception? Government finances, where rising interest costs and structural spending continue to quietly erode flexibility. Of course, stability in markets rarely lasts uninterrupted. Geopolitical tensions, particularly in energy-sensitive regions, serve as a reminder that inflation can reaccelerate quickly when supply shocks enter the picture.

Markets reflected this mixed backdrop in Q1. Equities stumbled, finishing down roughly 4% before a last-minute rally spared a worse outcome. Fixed income offered little relief, posting another disappointing quarter as higher rates continued to weigh on returns.

Meanwhile, beneath the headlines, several longer-term trends remain firmly in place. Private credit continues to deliver consistent income, offering a meaningful yield premium over traditional investment grade bonds. At the same time, large institutions are increasingly incorporating private markets into defined contribution plans—an evolution that raises both opportunity and important structural questions.

And finally, one structural shift worth noting: the U.S. is now a net energy exporter, fundamentally changing how global shocks impact the domestic economy.

Highlights

Q4 GDP revised downward to 0.7% (most blame falls on the government shutdown)

Inflation moderating - 2.4% - led by falling shelter costs

Unemployment at 4.4%

"Mandatory/non-discretionary" spending now 75% of federal budget

U.S. equities declined ~4% in Q1, despite a late-March rebound

Technology down 9.4% for the quarter, but still up 31.5% over the past year

Small caps now leading large over the past year

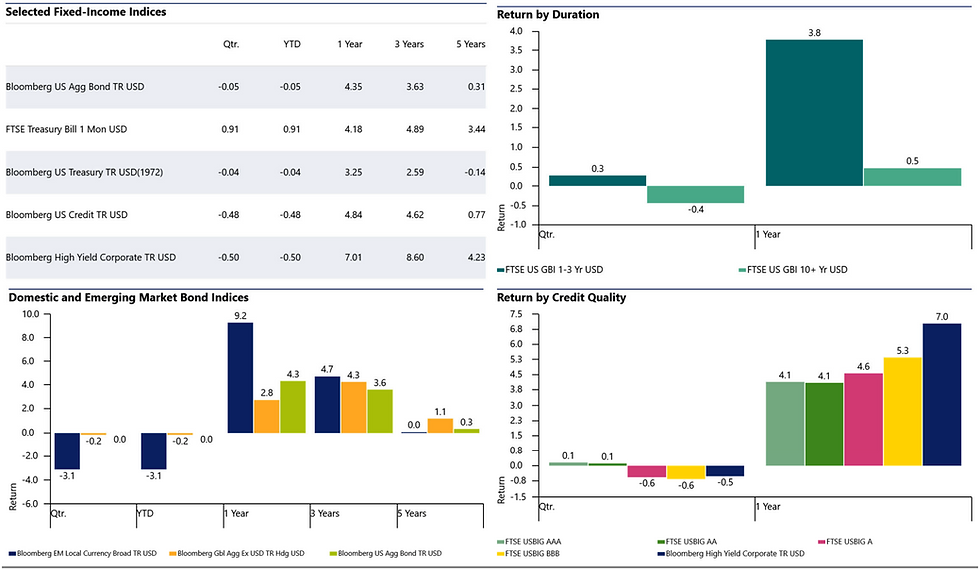

Domestic bonds down 5 bps in Q1

Short term bonds rose 30 bps for the quarter and 3.8% over the past year

Long term bonds down 40 bps for the quarter and up 50 bps over the past year

Commodities increased an outstanding 24% in Q1

Infrastructure up 11% in Q1

Hedge strategies quietly rose just under 2% in Q1

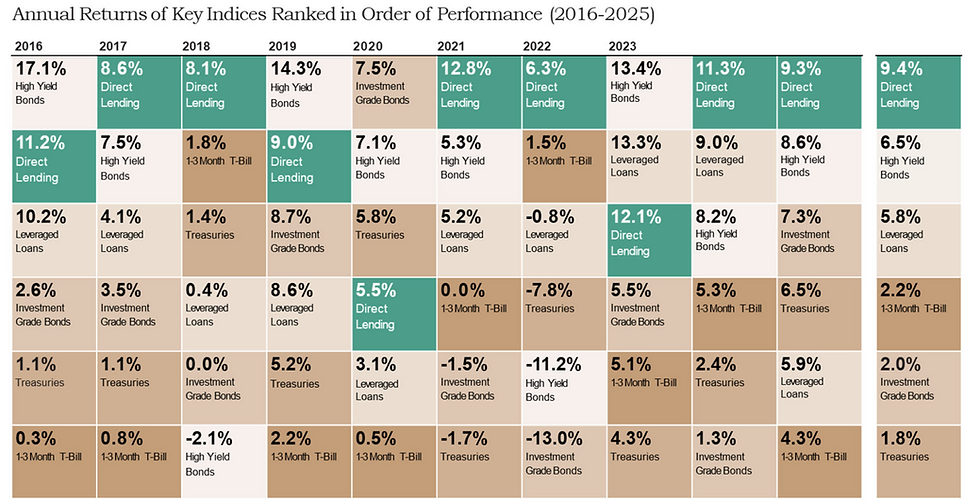

Private credit continues to deliver ~300–400 bps yield premium over IG bonds

Inflation Components

Shelter inflation - the heavyweight of CPI - is finally easing, helping pull headline inflation down toward the mid-2% range. A welcome shift after doing most of the heavy lifting over the past two years. However, before anyone declares victory, expectations are already resetting, with economists forecasting inflation to drift back toward ~3.5% by year-end.

Inflation, it seems, doesn’t disappear - it rotates across categories. Bottom line: progress is real, but the path forward remains uneven and far from settled.

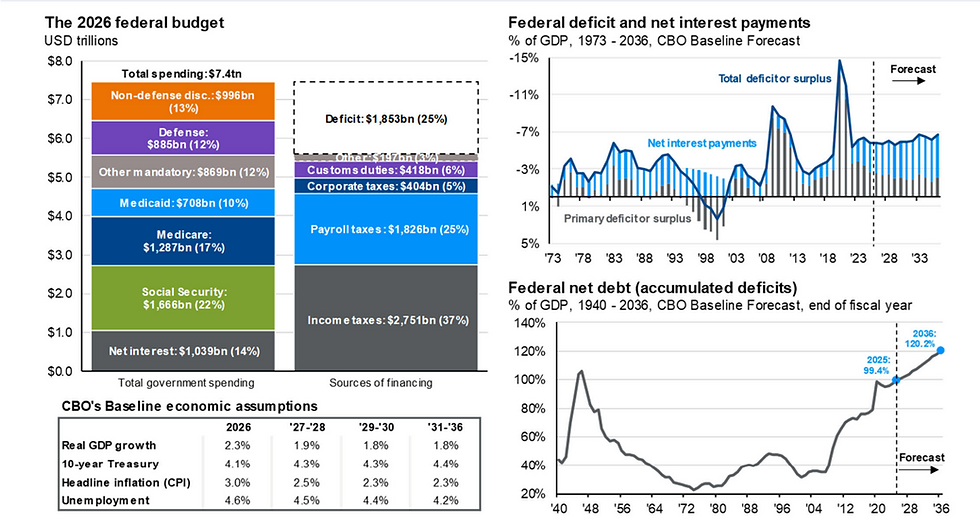

Federal Finances

Net interest expense has surged, from roughly 5% of federal spending prior to 2021 to 14% today. That’s a dramatic shift in a very short period of time, and it’s not slowing down.

At the same time, “mandatory” spending now accounts for roughly 75% of the federal budget, leaving limited room for discretionary decisions. Translation: most of the budget is effectively on autopilot, while the fastest-growing expenses are seemingly untouchable.

Flexibility is shrinking, and increasingly, the math - not policy - is in control.

Direct Lending: Performance in Context

Despite the steady drumbeat that private credit is “cracking,” the data tells a different story. Direct lending has delivered consistent, competitive returns - most often outperforming traditional fixed income.

Today, yields near ~9.5% stand in stark contrast to roughly ~4% for the broad U.S. bond market. Even more notable, long-term loss rates have remained below 1%, with recoveries around 50%.

Bottom line: for investors seeking income with discipline, semi-liquid private credit continues to look less like a risk and more like a solution.

Private Investments in Retirement Plans

Private markets are making their way into DC plans, with some providers suggesting allocations approaching 20% within TDF structures. The logic is sound - enhanced diversification and higher income potential.

But one question lingers: how does illiquidity behave in a daily-priced, daily-liquid environment during periods of stress? Smoothing works both ways - until it doesn’t.

Bottom line: the opportunity is compelling, but execution, liquidity management, and participant behavior will determine whether this evolution succeeds or fails.

Global Energy Trends

Geopolitical tensions tend to spark the same fear trade - oil spikes, inflation worries, and recession chatter. But structurally, the U.S. is in a very different position today. Back in 2006, fossil fuel imports accounted for roughly 30% of domestic energy needs and about 3% of GDP.

Today, the U.S. is a net exporter, with imports now negative - around -11% of consumption.

Meanwhile, Europe and China remain heavily import-dependent. Bottom line: energy shocks still matter - but far less here than abroad.

2025/2026 Retirement Plan Contribution Limits

2026 Tax Rates

Performance - Equities

After a strong run, Q1 delivered a reminder that markets don’t move in straight lines. Domestic equities slipped modestly, with most sectors in the red - technology included - while defensive areas offered little refuge.

International markets were similarly uneven, masking what had been strong trailing one-year returns. In other words, the leaders paused, but didn’t disappear.

Bottom line: short-term volatility has returned, but the longer-term trend still reflects a narrow group of winners carrying much of the load.

Performance - Fixed-Income

Q1 offered little relief for bond investors. Broad fixed income markets were essentially flat to slightly negative, with credit and high yield modestly trailing, while short-duration instruments quietly held their ground.

Longer-duration bonds continued to struggle as rates remained stubbornly elevated. The only reason one-year returns still look respectable is due to the two FOMC rate cuts providing a temporary boost.

Bottom line: bonds remain a difficult asset class - less risk than equities, but far from the risk reducer they once were.

Performance - Real Assets

So-called “alternatives light” delivered a mixed but telling quarter. Commodities did what they tend to do - surprise to the upside - posting strong gains thanks to the Iran conflict, while infrastructure held steady and hedge fund strategies quietly produced modest positive returns.

Real estate, however, continued to lag under the weight of high correlations to stocks. These are not home runs - they’re stabilizers.

Bottom line: liquid alternatives, with all their limitations, continue to quietly earn their seat at the table.

Comments