Well…this is getting uncomfortable.

- David Halseth

- Mar 22

- 2 min read

For the week ended 3/21/26.

And no, I’m not talking about your March Madness bracket getting torched by Thursday afternoon – I’m referring to the steady drip of losses across the markets. At this point, public market diversification feels less like a strategy and more like group therapy.

Before we get to that, let’s start with the Federal Reserve. As expected, the Fed held rates steady last week. No surprises – but the tone mattered. Powell made it clear they’re in no rush to cut, describing policy as sitting near “neutral.” That sounds nice in theory, but in practice it means they’ve got limited room to act unless something weakens…or breaks, which is usually how this movie ends.

Complicating matters? Energy prices. Rising tensions in the Middle East are pushing them higher – exactly the kind of inflation the Fed can’t control and doesn’t want. The vote was 11–1 to hold, which basically translates to: “we’re fine…we think.”

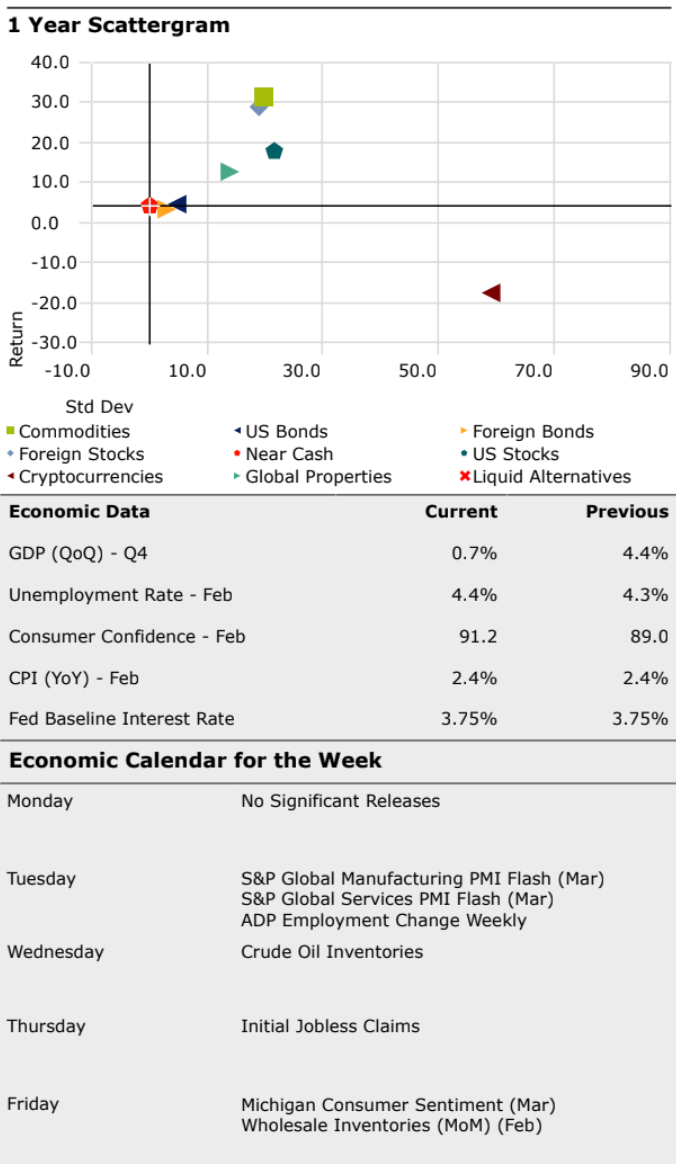

Meanwhile, the bond market continues to ignore its job description. The 10-year Treasury climbed to 4.4%, and bonds – yes, the supposed safe haven – are quietly in another bear market. Down 51 basis points last week and now off 68 basis points on the year. Not catastrophic, but let’s be honest – when things get shaky, bonds are supposed to help. Lately, they’ve been more “spectator” than “shock absorber.”

Equities didn’t fare much better. U.S. stocks fell 1.9% on the week, with international down 2.2%. Year-to-date, U.S. markets are now off 4.3%, while international is down 1.4%. So much for that overseas momentum – turns out narratives, like milk, have expiration dates.

The real driver here is Iran. The Strait of Hormuz remains one of the most critical choke points in global energy, and markets are now forced to price in that risk. Oil reflects it immediately. Natural gas, however, tells a more interesting story – surging in Europe while staying relatively stable in the U.S. The difference? Energy self-sufficiency. It’s not flashy, but it matters, a lot, when things get messy.

Looking ahead, we get PMI data Tuesday and consumer sentiment Friday. Of the two, sentiment may matter more. When confidence cracks, everything else tends to follow shortly behind.

So where are we? The Fed is stuck in neutral. Bonds aren’t behaving. Stocks are under pressure. And geopolitics is doing what it always does – showing up uninvited and overstaying its welcome.

In other words, volatility is back.

Enjoy your morning coffee. Maybe make it a double.

Interesting data point of the week.

Comments