Europe Rises While the U.S. Stumbles

- David Halseth

- Mar 9, 2025

- 2 min read

For the week ended 3/8/2025.

Jobs: Hiring Increases as Does Unemployment

First, the good news—the U.S. economy kept adding jobs at a steady pace last month. According to the Labor Department, a seasonally adjusted 151,000 positions were created in February, slightly below the 170,000 forecast (when was the last time economists nailed a forecast, anyway?). More importantly, that’s an improvement over January’s 125,000.

Now for the downside—the unemployment rate ticked up to 4.1% from 4.0%. And no, it wasn’t due to all the headlines about federal layoffs, as most of those came after the data cutoff. That said, the report did show a 10,000-job loss in the federal government, with 3,500 from the Postal Service and the remaining 6,500 representing the biggest drop in two years. Interestingly, at the state and local level, 20,000 jobs were added, about half in education. Clearly, much more to come on this front.

Now, back to those ever-pessimistic economists. The consensus view is that a combination of federal job cuts, reduced government funding, and trade uncertainty will weigh on employment growth in the coming months. And they wonder why it’s called the dismal science. Thank you, Thomas Carlyle.

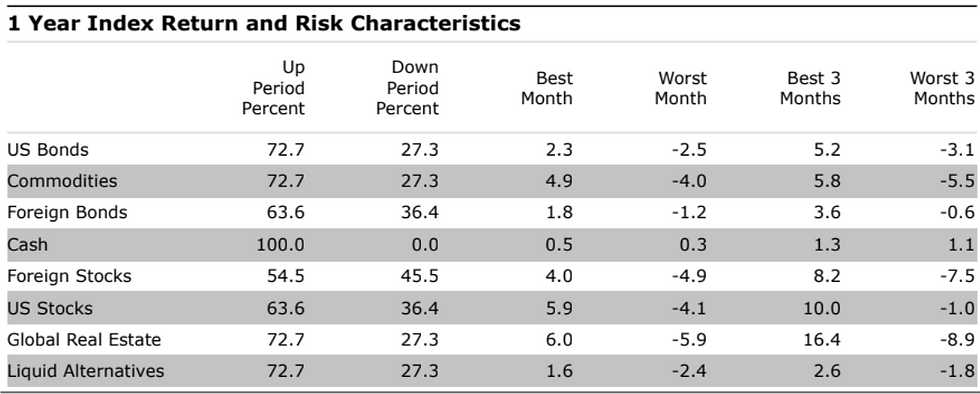

Market Divergence: U.S. vs. The World

The divergence between U.S. and international stocks in 2025 is becoming more pronounced. Last week, U.S. equities fell another 3.1%, while international markets gained 2.6%. Year-to-date, global stocks are up 8.3%, while the S&P 500 is down 1.7%.

What’s driving this? The narrative (isn’t it always about the narrative?) is that chaos in Washington, D.C. is rattling U.S. markets, while overseas, European Central Bank (ECB) rate cuts are lowering borrowing costs and fueling optimism. Apparently, European investors are tuning out Germany’s two-plus years of negative GDP growth, the war in Ukraine, and other pressing issues. But hey, selective optimism is a powerful thing.

Oh, and bonds lost money again last week. Just in case anyone was feeling too cheerful.

Looking Ahead: CPI in Focus

The key data point to watch this week? Wednesday’s CPI release. The consensus expects a slight dip to 2.9%, but I wouldn’t bet the farm on it. Sticky services inflation, energy prices, and wage pressures could easily throw a wrench in those hopes.

And with that, may you have a productive Monday and pay a tad less attention to the circus in Washington, D.C. After all, what we do on a personal level matters far more than anything happening “back east.”

Good morning.

Interesting data point of the week.

Comments